Asana S1 interesting facts

After a long time, I decided to read a S1. Used this new framework to read S1's.

Most of the content is structured in bullet points for faster consumption. Also, most of the content are quoted directly from their S1.

Introduction

History - The founders faced the problem firsthand at Facebook.

1.2 mil paid users. 75k paying customers. 143 Mil USD Annual revenue.

3.2 mil free activated accounts (since inception). ~25 Mil users.

"Today, 60% of knowledge workers’ time is spent on work about work."

"Despite the growth in collaboration technology such as content tools and messaging apps, there has been little innovation in work management—systems that help teams to plan, manage, and execute their work." → I find this hilarious.

As customers realize the productivity benefits, we provide, our platform often becomes critical to managing their work and achieving their objectives, which drives further adoption and expansion opportunities. This is evidenced by our dollar-based net retention rate, which increases with greater organizational spend. As of January 31, 2020, our dollar-based net retention rate within organizations spending $5,000 or more with us on an annualized basis was over 125%, consisting of 6,555 customers. Our dollar-based net retention rate within organizations spending $50,000 or more with us on an annualized basis was over 140%, consisting of 207 customers. Our overall dollar-based net retention rate as of January 31, 2020 was over 120%.

Seven hundred employees

"The average knowledge worker receives 121 emails per day—70% of which are opened within six seconds."

Spreadsheets are Asana's biggest competitors.

Asana looks at 3 categories of users - Individuals, Team leads, Executives. This is interesting that their preferred division is not just organizations BUs, verticals but instead individual v/s team leads v/s executives.

Our free-to-paid conversion rate of registered users, as measured by the number of paid users divided by the total number of then-registered users, has increased from 3.6% as of January 31, 2018 to over 4.8% as of January 31, 2020.

Growth - We also see a large opportunity to expand our international customer base. For fiscal 2020, 41% of our revenues came from international regions, with limited dedicated sales effort and no product customization outside of limited language translation and multi-currency capabilities. Within the past 12 months, we have opened offices in key regions across Europe and Asia, and expect to grow our customer base within these areas.

Asana is hosted on AWS.

No individual customer represented more than 1% of Asana's revenues.

Our “work graph.” Like the social graph the two of us helped create for Facebook, the work graph is a flexible data model—of people, tasks, goals, projects, portfolios, conversations, files, and the relationships among them—powering Asana. The work graph enables each Asana user to see information in the format that makes most sense for them.

Financials

We introduced Enterprise subscriptions and Business subscriptions in December 2016 and November 2018, respectively. These subscriptions have grown to represent approximately 42% of our revenues during the three months ended January 31, 2020, up from 11% during the three months ended January 31, 2019.

We have also experienced a shift to larger subscriptions, with subscriptions of over $5,000 representing 54% of our revenues for the three months ended January 31, 2020, compared to 43% for the three months ended January 31, 2019.

Of our 100 largest customers today, virtually all came to Asana using a free trial of our paid levels or through an upgrade from our Basic level.

Over 30% of Fortune 500 companies use Asana.

No single customer accounted for more than 1% of our revenues, and our top 100 customers accounted for approximately 9% of our revenues for fiscal 2020. For fiscal 2020, 41% of our revenues were generated outside the United States with limited international sales presence or major product customization.

By providing a free version of Asana, a free trial option, and a feature where customers can invite guests outside of their organizations to use Asana, we are able to seed the market with Asana users. Once individuals and teams within organizations adopt our platform, our direct sales team follows up with an opportunity to strategically expand our offerings across the organization. We are at the early stages of building our direct sales force to focus on the significant expansion opportunity we see within our customer base.

For fiscal 2020, our payback was 10.6 months, and for the 12 months ended April 30, 2020, it was 11.4 month.

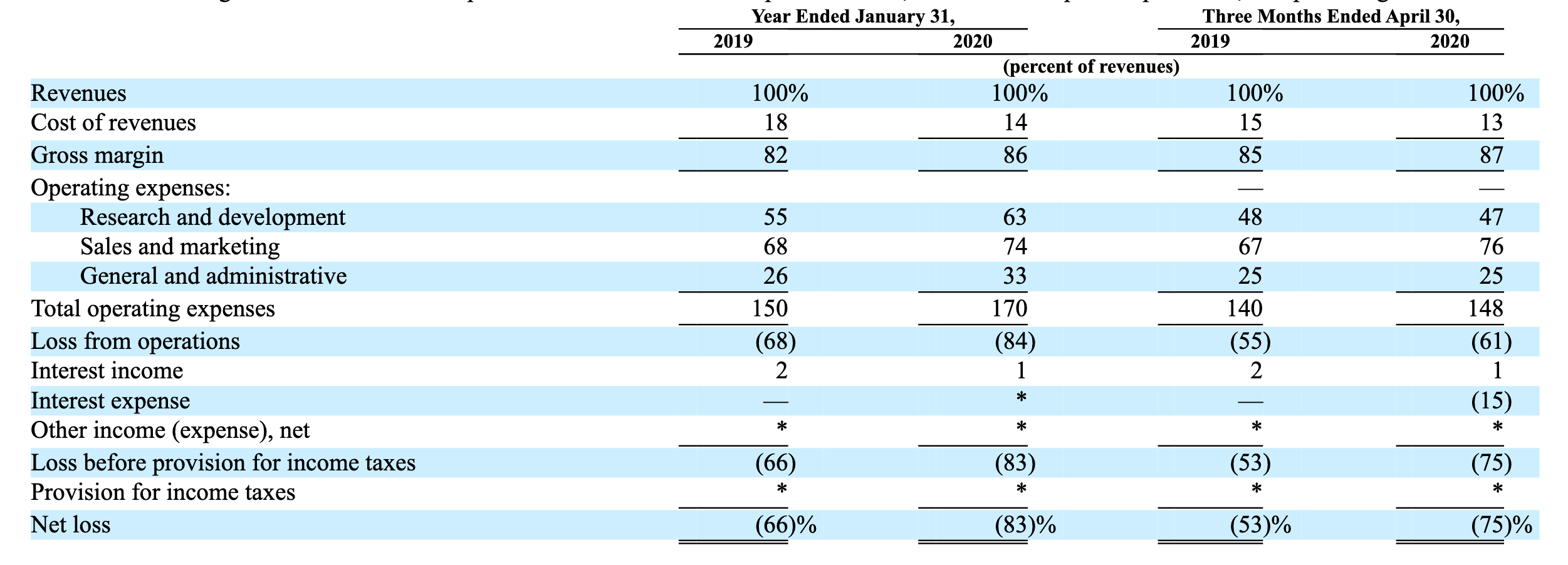

Results of operations -

Cost of revenues increased $2.1 million, or 51%, during the three months ended April 30, 2020 compared to the three months ended April 30, 2019. The increase was primarily due to an increase of $0.7 million in third-party hosting costs as we increased capacity to support customer usage and growth of our customer base, $0.6 million in personnel-related costs due to increased headcount, $0.4 million in allocated overhead costs as a result of increased overall costs to support the growth of our business and related infrastructure, and $0.4 million in credit card processing fees.

Research and development expenses increased $9.0 million, or 67%, during the three months ended April 30, 2020 compared to the three months ended April 30, 2019. The increase was primarily due to an increase of $6.9 million in personnel-related expenses driven by higher headcount and an increase of $1.7 million in allocated overhead costs as a result of increased overall costs to support the growth of our business and related infrastructure.

Cost of revenues increased $6.0 million, or 44%, for fiscal 2020 compared to fiscal 2019. The increase was primarily due to an increase of $3.6 million in third-party hosting costs as we increased capacity to support customer usage and growth of our customer base, $1.6 million in personnel-related costs due to increased headcount, and $1.5 million in credit card processing fees, partially offset by a $0.7 million decrease in amortization of capitalized internal-use software costs.

Our gross margin increased for fiscal 2020 compared to fiscal 2019 as we increased our revenues and more efficiently managed third-party hosting costs, realized benefits due to economies of scale resulting from increased efficiency with our technology and infrastructure, and experienced a decrease in amortization of capitalized internal-use software costs.

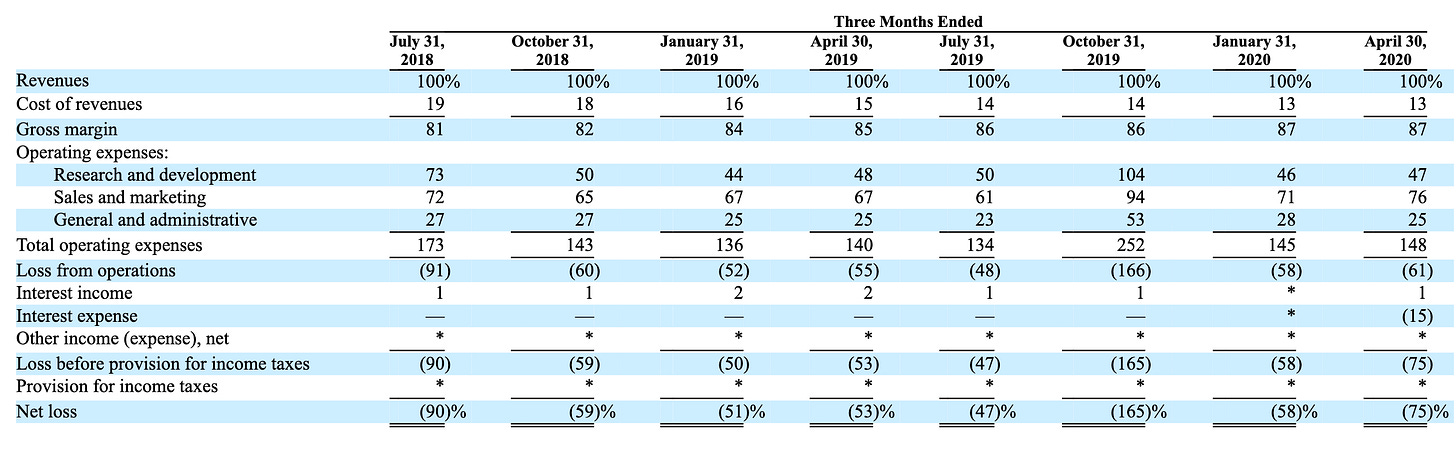

No majorly quarterly trends stand out.

Liquidity and Capital Resources

Asana has spent a total of 365 mil USD till date. Raised 214 mil USD of external capital.

In Apr 2020, they raised 40 mil USD in loan from SVB to build their headquarters. (wrong time? Covid? Work from home?)

A substantial source of our cash provided by operating activities is our deferred revenue, which is included on our consolidated balance sheets as a liability. Deferred revenue consists of the unearned portion of billed fees for our subscriptions, which is recorded as revenues over the term of the subscription agreement. As of January 31, 2020 and April 30, 2020, we had $64.1 million and $70.1 million of deferred revenue, respectively, of which $62.7 million and $68.6 million, respectively, were recorded as a current liability.

Contractual Obligations and commitments

In February 2019, we entered into a new lease agreement for our corporate headquarters in San Francisco. This lease commenced in May 2020 and expires in October 2033. As part of the agreement, we issued a $17.0 million letter of credit upon access to the office space. We expect to start making recurring rental payments under the lease in the second quarter of fiscal 2022. We have begun participating in the construction of the office space and will incur construction costs to prepare the office space for its use, which will be partially reimbursed by the landlord. As of January 31, 2020, the future minimum payments and capital commitments related to this lease, which include tenant improvement allowances of $26.6 million, totaled $466.0 million. Subsequent to January 31, 2020, we incurred a delay associated with the construction of the office space, and as a result, we expect to incur a total of $457.4 million of future minimum payments and capital commitments as of April 30, 2020. Additionally, in April 2020, we amended the lease arrangement to include additional space, for which future minimum payments total $3.9 million. Our CEO acts as a personal guarantor to the lease for the full rent payments over the 148-month term should we default on our obligations. These amounts are not included in the table above.

Executive compensation | Certain relationships and related party transactions

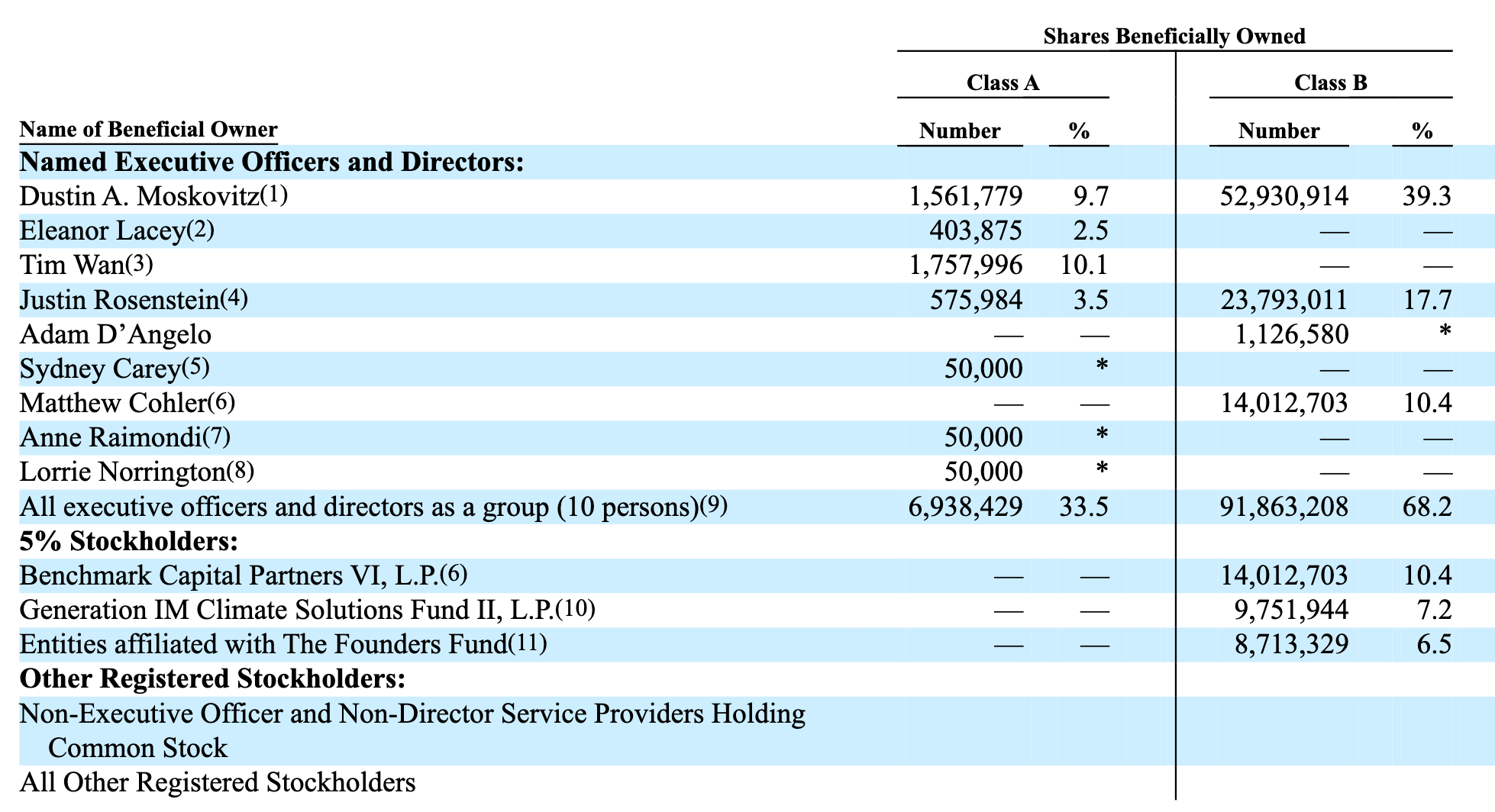

Dustin Moskovitz transferred a bunch of his shares to a trust

Cap table summary

Some Miscellaneous Thoughts -

Asana's dollar-based net retention rate increases with greater organizational spend.

Spreadsheets are Asana's biggest competitors. Surprising that people have repurposed spreadsheets for this!

Asana looks at 3 categories of users - Individuals, Team leads, Executives.

The competition section brushes off everything.

The first thing I see when I sign up on Asana is a maintenance tab that Asana will have a 2-hour planned downtime. This is surprising 😔

Of our one hundred largest customers today, virtually all came to Asana using a free trial of our paid levels or through an upgrade from our Basic level. - Highlights the importance of having free trials?

Attended an interesting conversation hosted by Ankit from Product folks. Learnt some lessons of evolution of Asana as a product -

Learnings from webinar

Generic point when companies go public - Average around 150M LTM recurring revenue

Asana started from Tasks (internal PM tool developed in Facebook)

Rosenstein and Moskovitz left Facebook to start Asana

Dropbox was launched in private with 75k user waiting lists.

In 2009, 5 people, 9mil USD from benchmark and A16Z.

Asana was always trending in hackernews, quora etc. Evangelised well by their founders.

Asana was finally launched in 2011. 1200 companies in waiting list. It was a very horizontal application.

First paid plan for them was a tier based on number of users (<30, 30-50 etc instead of having a per user plan).

Asana went after internal emails (like Slack).

Thought - World moves in small jumps. Even Email to Asana was too big, people preferred email to slack.

Miscellaneous fact - Slack's co-founder is Flickr's co-founder.

Asana was one of the first collaboration software to add calendar.

But the common problem was that UI was pretty clunky.

In 2015, they revamped a new UI. Existing customers hated it (it was like new Coke, where existing users of Coke hated it). Lesson for Asana is that don't introduced a big rebrand at once, make continuous minor tweaks.

In 2016, Asana launched boards to compete against Trello.

Possible Discrepancies -

Asana mentioned in Sept 2018 that they had 50k paying customers on the blog, but in S1 said >32k.

"paid" customers v/s paying customers → Churn might have been ignored.

Competitor →

Smartsheet is a direct competitor (like airtable, a few years behind).

Dropbox was a product led growth. Almost close to a consumer app...

2.2% free to paid is not bad for a product led growth.

People start free and sales teams go in when 50-60 users.

Asana is a very team based product, whereas slack is organisational level. Hence the spend is a lot larger for the latter.

Will publish some interesting facts from Unity S1 soon (next weekend hopefully)!